Energy storage has emerged as a cornerstone technology for clean energy transitions globally. As power systems incorporate higher shares of variable renewable energy, maintaining reliability requires the ability to balance supply and demand across time. In India, where the target is 500 GW of non-fossil electricity capacity by 2030, this balancing challenge is becoming increasingly central. India’s energy storage requirement is expected to rise five-fold, with some projections suggesting 411.4 GWh by 2031–32, underscoring the scale and pace at which storage technologies will need to be developed and deployed. To adequately support high renewable penetration, system adequacy, and grid stability, grid-scale storage power capacity could reach up to 178 GW by mid-century, according to net-zero-consistent power-system modelling.

Energy storage technologies differ not only in the medium used to store energy, but also in the time scales, services, and system roles they are designed to perform, as well as the required research, development and demonstration (RD&D) needs. For instance, electrochemical storage1 dominates short- to medium-duration (15 minutes to <8 hours) applications where fast response, modularity, and ease of deployment are critical. Meanwhile, mechanical2, thermal3, and chemical4 storage technologies tend to serve longer-duration (> 8hours to days) or system-level roles, such as bulk energy shifting, inertia provision, or seasonal balancing, but are often more site-specific and infrastructure-intensive. In parallel, enabling layers, including power electronics, control systems, and software, cut across storage technologies and play a critical role in determining how effectively storage assets interact with the grid. These technologies differ from most other clean energy technologies in three ways.

Firstly, storage technologies do not generate energy; they provide flexibility. Their value lies in services such as peak shaving, frequency regulation, voltage support, reserve provision, and congestion management. As a result, storage performance cannot be assessed independently of the power system in which it operates. This contrasts with solar or wind technologies, where performance improvements are largely intrinsic to the device.

Secondly, storage technologies operate across multiple time scales. Storage must respond in milliseconds to stabilise the grid, operate over a few hours to shift solar power to evening peaks, and potentially store energy for longer periods in the future, particularly to manage multi-day renewable variability or extended supply shortfalls. Because no single technology can meet all these needs, storage RD&D naturally spans multiple approaches rather than converging on one solution.

Lastly, current storage technologies face a distinctive degradation problem. Unlike generation assets, storage systems, especially batteries, degrade with every charge–discharge cycle and even when they are not in use, requiring continuous RD&D to manage performance loss, safety risks, and lifespan reduction. These challenges are further amplified in India, where temperatures frequently exceed 40°C. For instance, a lithium-ion battery stored for one year at 40°C will drop to 65% of its full capacity even when stored and left unused.

These differences are not merely technical; they shape how storage RD&D is structured and funded. Public portfolios inevitably reflect choices about which system needs are prioritised and which technologies are considered ready for scale. Examining India’s public storage RD&D portfolio, therefore, offers insight into how the country is balancing near-term deployment needs with longer-term system transformation.

What India’s storage RD&D portfolio signals

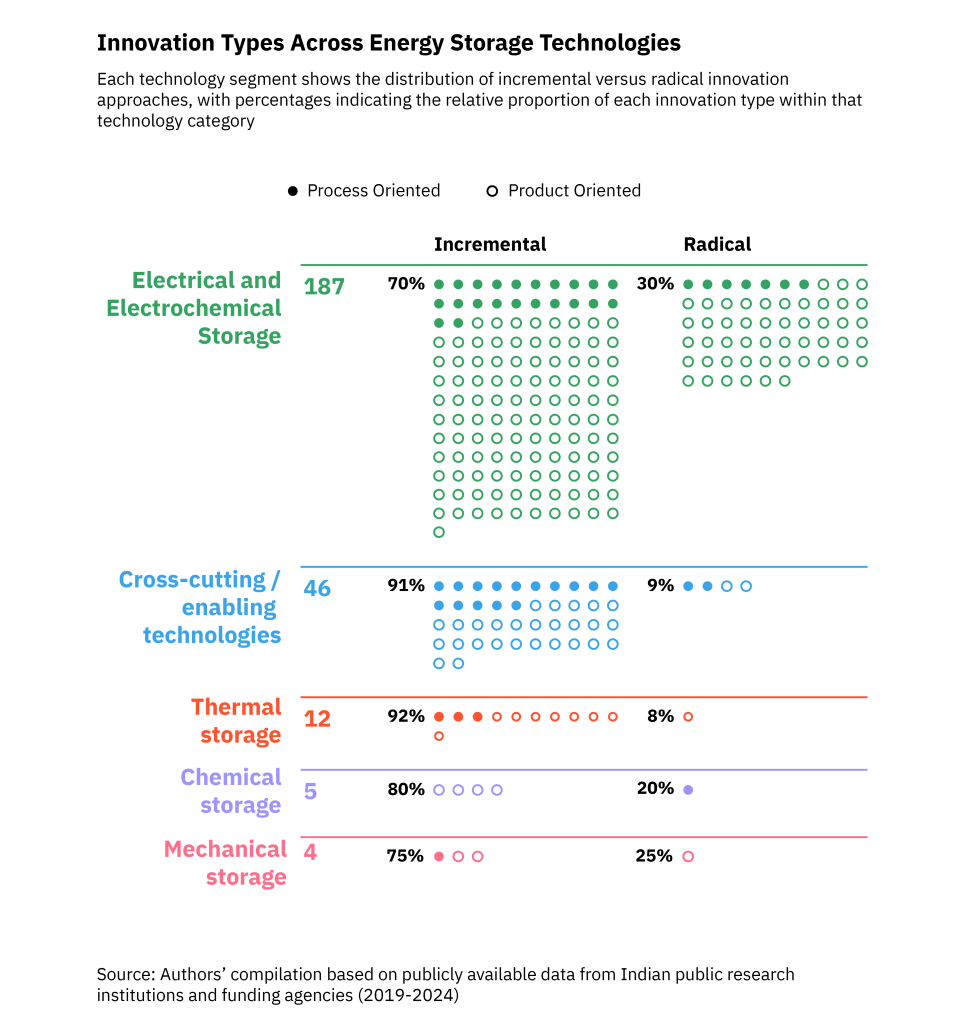

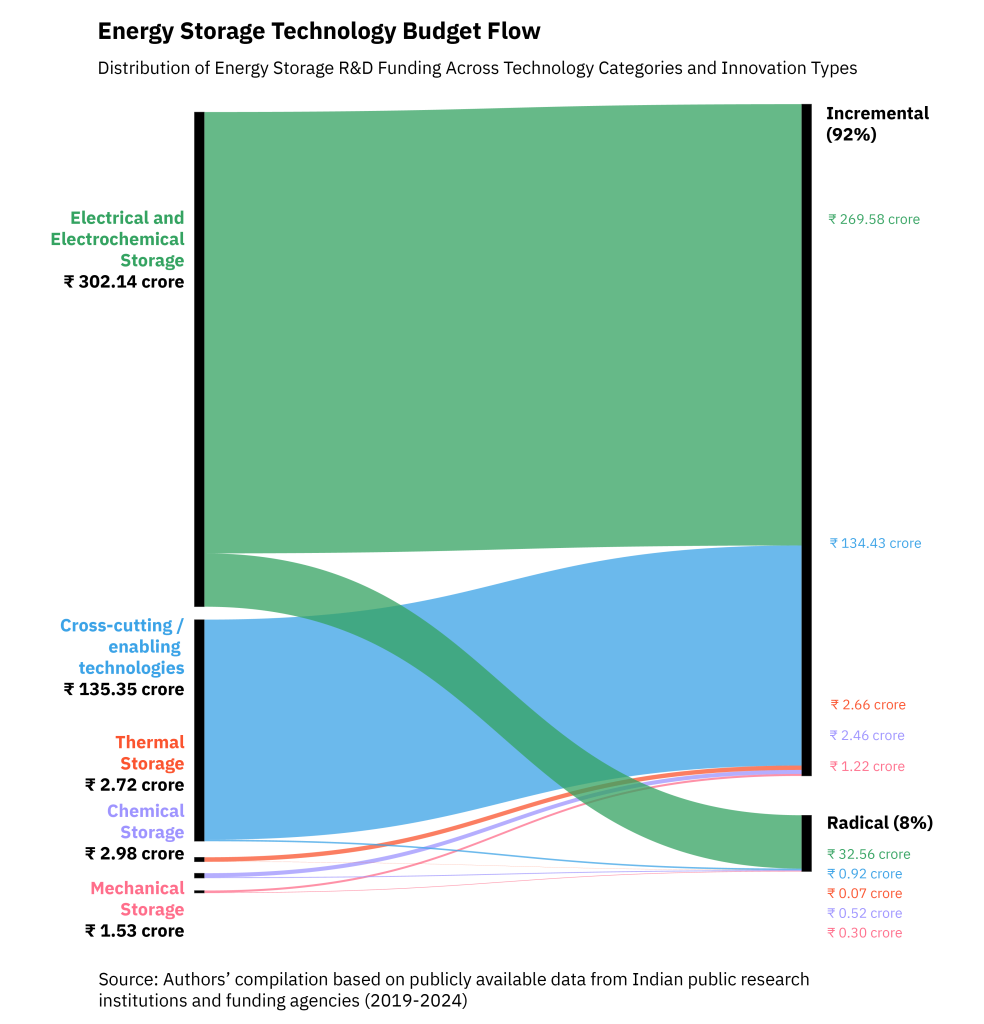

Our review of India’s public energy storage RD&D portfolio reveals a highly concentrated innovation strategy, centred overwhelmingly on electrochemical batteries and shaped by near-term system needs and industrial priorities. Our analysis focuses on publicly funded energy storage RD&D, given its central role in shaping technology trajectories, early-stage research, risk-sharing, and capability-building in India. At the same time, private firms are increasingly active with a growing start-up landscape emerging across the battery energy storage systems (BESS) value chain, from alternative chemistries and battery pack manufacturing to battery management systems (BMS) and battery-as-a-service models, signalling growing private-sector innovation alongside deployment.

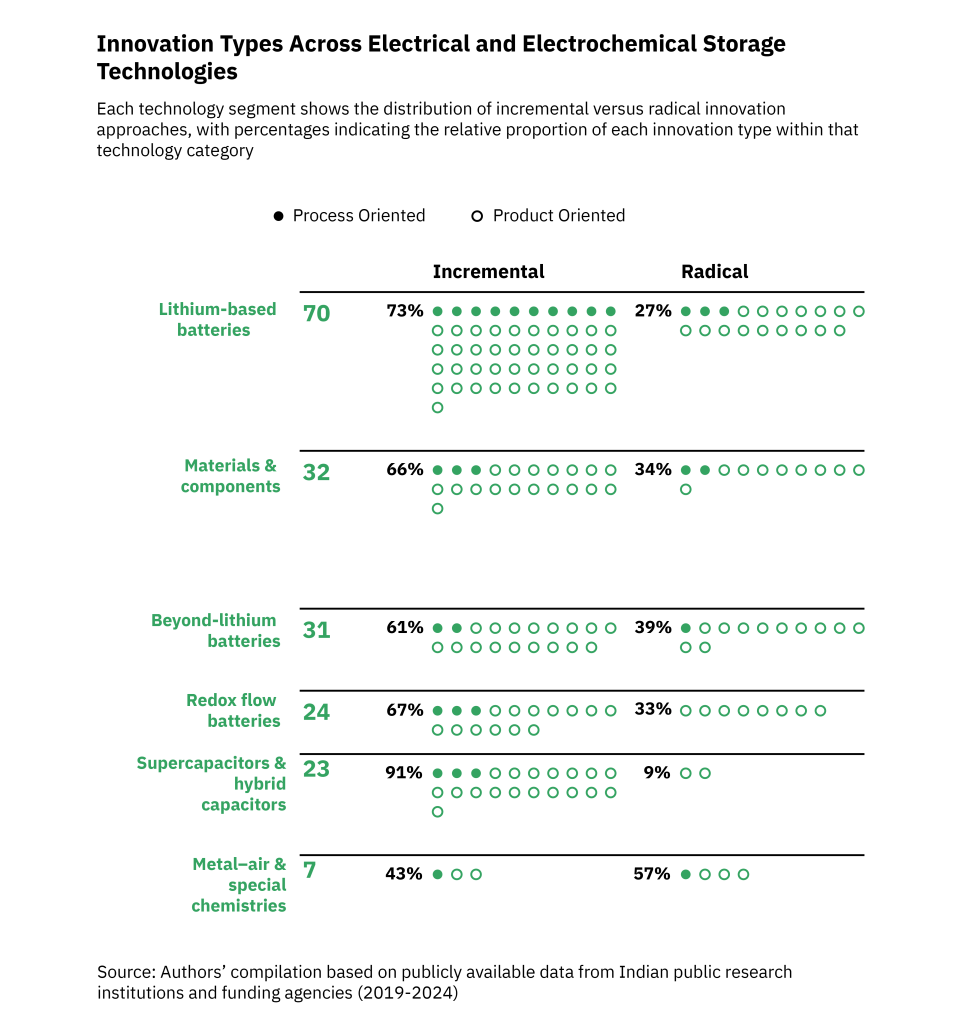

Across the portfolio of over 250 projects, electrochemical and electrical account for more than four-fifths5, with lithium-ion technologies forming the core. These projects focus primarily on incremental improvements to electrode materials, electrolytes, thermal stability, and cycle life, which influence performance, safety, and manufacturability. This emphasis reflects the dual role batteries play in India’s transition: they are both critical to electric mobility and as the most immediately deployable option for short-duration grid storage. While electric mobility and stationary storage batteries differ in performance requirements and, in some cases, chemistry choices, there are important areas of industrial overlap. Cell manufacturing, materials processing, pack assembly, battery management systems, and power electronics form a shared capability base. As India scales up advanced chemistry cell (ACC) manufacturing to meet demand across mobility and power sectors, learning effects and industrial spill-overs are likely to shape innovation trajectories in both domains.

While lithium-ion clearly dominates the portfolio, a smaller but visible set of projects explores alternative chemistries, including sodium- and aluminium-based systems grouped under the beyond-lithium battery category6 in the visual above, as well as redox flow batteries7. Their presence indicates growing awareness of geopolitical and mineral constraints, cost pressures associated with lithium-based systems, and of leveraging India’s relative advantage in sodium availability. Efforts are aimed towards reducing costs, improving efficiency, and developing India-centric designs. However, research into these technologies largely mirrors lithium-ion research in its orientation, focusing on device- and component-level innovation such as materials synthesis and performance benchmarking, rather than being embedded in a broader strategy for long-duration or grid-specific storage applications.

Public institutions such as Indian Institutes of Technology (IITs), Indian Institute of Science (IISc), Bengaluru, Central Electrochemical Research Institute (CECRI), and International Advanced Research Centre for Powder Metallurgy and New Materials (ARCI) are active across battery-focused research areas, alongside DST-supported projects on alternative chemistries and materials.

Beyond batteries, the portfolio thins out rapidly. Thermal energy storage8 appears in a small but meaningful subset of projects, suggesting some engagement with non-battery storage pathways. Yet these projects remain largely disconnected from discussions around industrial heat, renewable integration, and system flexibility, and are treated as standalone research topics.

More striking, however, is the near-absence of long-duration storage technologies. Project-level engagement with pumped hydro9 innovation, compressed air energy storage10, or gravity-based systems11 is minimal. This is notable given India’s significant pumped hydro potential of 176 GW and emerging concerns around grid inertia as solar penetration increases. This pattern does not necessarily imply that long-duration storage is unimportant. Rather, many of these technologies are highly site-specific and infrastructure-intensive, with feasibility shaped more by geography, land and water availability, permitting, and system planning than by laboratory-scale or component-level innovation. As a result, these technologies tend to be approached primarily as planning and project development challenges, rather than as domains where sustained public RD&D is viewed as the binding constraint.

Is India’s battery-first approach to storage a problem?

This focus on batteries raises a familiar question we have explored in earlier blogs on solar energy and green hydrogen in this series: Does India risk narrowing its innovation options by focusing so heavily on batteries? Or is this emphasis a rational response to India’s needs and global technology trajectories?

India’s battery-centric approach is not an outlier. Globally, BESS accounts for the overwhelming majority of new storage deployments and RD&D investment through 2030. In 2025, global investment in batteries for power sector storage is projected to have exceeded USD 66 billion with total installed battery storage capacity reaching 258 GW. Meeting the 2030 goal of tripling renewable energy will require a six-fold expansion of energy storage worldwide, with batteries expected to account for nearly 90% of new capacity additions and other technologies providing supplementary support. Such rapid scaling is largely enabled by declining battery costs. Utility-scale battery storage costs in 2024 fell to about USD 192/kWh, a roughly 93% decline since 2010, making batteries the most competitive option for short- to medium-duration storage.

Even in countries actively funding long-duration energy storage research, batteries continue to dominate near-term deployment because they are modular, quick to deploy, and compatible with existing grid architectures. China illustrates this pattern, combining large investments in pumped hydro with a near fourfold expansion in battery storage capacity in recent years. Similarly, Australia has rapidly expanded BESS but is investing heavily in non-battery storage in parallel, most notably through large pumped hydro projects designed to deliver long-duration energy shifting and system adequacy.

India’s energy storage RD&D strategy can therefore be seen as reflecting a near-term pragmatic reading of current system needs, global cost curves, and institutional constraints rather than a judgment about the technologies that will matter over the full course of the energy transition. By focusing on batteries, India is prioritising technologies that are commercially viable in the short-term, aligned with EV demand, and capable of scaling quickly to support renewable integration.

The question, therefore, is not whether India should shift away from batteries today but whether its storage innovation ecosystem retains the capacity to adapt as system needs evolve. Given current system conditions, rapid renewable scale-up, and the need for short- to medium-duration balancing, batteries remain the most practical and scalable storage option. The challenge for storage RD&D is not about correcting a misallocation in the present, but about ensuring that alternative pathways are not unintentionally side-lined as the power system becomes more complex beyond the early 2030s. In that sense, storage innovation is less about choosing a single winner and more about maintaining a portfolio that can respond to changing technical, economic, and system realities.

This blog is part of our Clean Energy RD&D Insights series, examining India’s evolving clean energy innovation landscape. Read the other blogs on green hydrogen here and solar energy here. We would also like to thank Kunal Agnihotri for his help in designing the visuals for this piece.

Endnotes

- Electrochemical energy storage systems store and release electricity through reversible chemical reactions within battery cells (e.g., lithium-ion, sodium-ion, redox flow) ↩︎

- Mechanical storage systems convert electrical energy into mechanical potential or kinetic energy (e.g., pumped hydro, compressed air, flywheels, gravity systems) ↩︎

- Thermal energy storage systems store energy as heat or cold in a medium (e.g., molten salts, water, phase-change materials) for later use in power generation or direct thermal applications ↩︎

- Chemical storage systems convert electricity into chemical energy carriers (e.g., hydrogen, synthetic fuels, ammonia) through processes such as electrolysis ↩︎

- In this analysis, electrical and electrochemical storage technologies are grouped together because they share similar innovation characteristics and RD&D pathways. Both rely on advances in materials science, power electronics, and system integration, and are typically deployed for short- to medium-duration applications requiring fast response times. In India’s public RD&D portfolio, these technologies are also funded, evaluated, and implemented through similar institutional and programmatic channels, making it analytically meaningful to examine them together ↩︎

- Beyond-lithium batteries category includes multiple chemistries such as sodium- and aluminium-based systems. These are grouped together as they represent alternative chemistries within broadly similar battery architectures. These technologies often target the same applications as lithium-ion systems, draw on comparable manufacturing processes, and face similar RD&D challenges related to materials performance, cost reduction, and scalability. Redox flow batteries and metal–air systems are treated as separate categories because they differ more fundamentally in design, operating principles, and innovation pathways ↩︎

- Besides lithium-ion batteries, flow batteries could emerge as a breakthrough technology for stationary storage as they do not show performance degradation for 25-30 years and are capable of being sized according to energy storage needs with limited investment ↩︎

- Thermal Energy Storage captures and stores heat or cold in a medium (like water, rock, or salt) for later use, balancing energy supply and demand ↩︎

- Pumped storage hydropower a large-scale energy storage method that uses two reservoirs at different elevations to act like a giant rechargeable battery, storing surplus electricity by pumping water uphill and releasing it downhill through turbines to generate power when needed ↩︎

- Compressed Air Energy Storage stores excess electricity by compressing air and storing it in underground caverns or tanks, releasing it later to drive turbines and generate power, effectively acting like a large battery ↩︎

- Gravity-based energy storage systems store excess electricity by lifting heavy masses (like concrete blocks or water) and release it by allowing them to fall, converting potential energy back into power using a generator, acting as a sustainable, long-lasting alternative to batteries ↩︎