India’s Union Budget announcements are an important annual signal of where the Union government is committing its scarce on-budget1 resources, such as subsidies, grants, and public investment, revealing the priorities and trade-offs it is willing to make. In particular, the 2026–27 announcement signals what the government intends to support domestically in the clean energy transition. Four announcements stand out. First, a $2.2bn push for carbon capture, utilisation and storage (CCUS), positioned as support for industrial decarbonisation and intended to reach multiple hard-to-abate sectors. Second, a renewed focus on critical and rare earth minerals, including a proposal to establish dedicated rare-earth corridors in Odisha, Kerala, Andhra Pradesh, and Tamil Nadu to promote mining, processing, research, and manufacturing. Third, customs-duty relief on imports of nuclear power equipment, with the exemption extended through 2035. Fourth, duty cuts for lithium-ion cells for battery storage and inputs for solar-panel glass manufacturing, thereby lowering input costs in key clean-tech supply chains. Alongside these, power-sector spending continues to point toward grid and integration enablers, including efforts often discussed through programmes like the Green Energy Corridor.

Taken together, these measures signal a push to strengthen domestic supply chains and the backbone needed for the clean energy transition. They may lower input costs, support domestic value chains, and invest in infrastructure that must carry a higher share of clean power. Realising this ambition will require an increase in overall funding; the key question, then, is what form that support would take and whether it is suited to addressing the relevant bottlenecks.

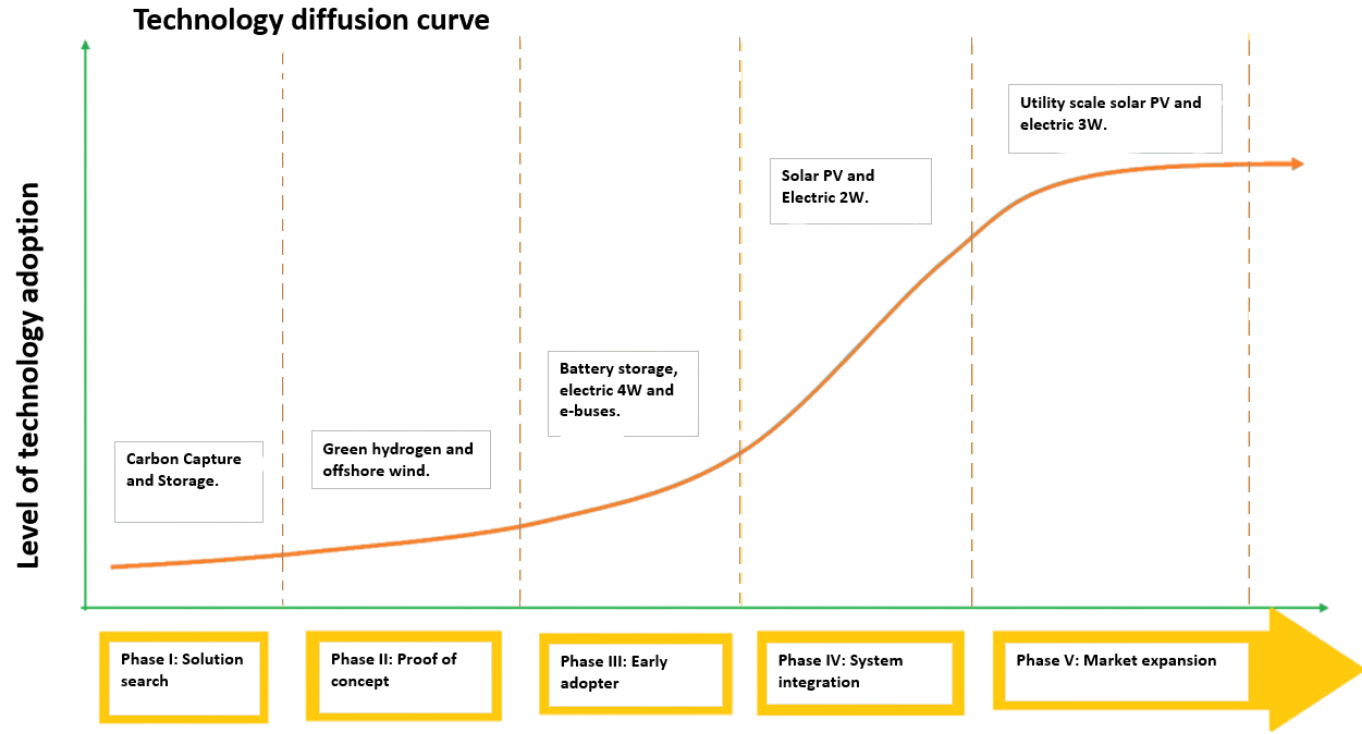

A Technology Diffusion and Finance Framework

Our research on clean technology diffusion begins with the premise that financing barriers and the types of financial support required vary across stages of their diffusion. What hinders a technology early is often not what holds it back later. To study this, we draw on the innovation systems approach, which assumes that any technology needs a supporting ecosystem to diffuse. It focuses on the ecosystem of actors (firms, researchers, financiers, government) and the rules and infrastructure (standards, regulation, procurement, networks) that together determine whether a new technology can develop, prove itself, and scale. Using this approach, we then map the range of policy instruments (fiscal and non-fiscal, as well as financial and non-financial) that governments use to support diffusion.

Existing literature commonly organises diffusion into five stages along an S-curve, from early research to market saturation. The innovation process typically begins with a Solution Search phase, when there are significant uncertainties about the technology’s future market potential. Private capital is hard to attract at this stage. Public support, therefore, tends to focus on early research and development – through grants and subsidies – to explore options and identify potential new solutions. Once viable options emerge, they proceed to the Proof of Concept stage, in which pilot projects are implemented to test feasibility in real-world conditions. If those efforts succeed, technologies enter the Early Adoption phase. At this stage, they have cleared major technical hurdles but are not yet commercially established. Policy support often focuses on enabling first-market entry and encouraging initial uptake. As deployment grows, System Integration becomes critical, a phase when the projects become attractive to institutional investors. The priority shifts to building enabling infrastructure and market frameworks so projects can scale reliably and attract larger pools of private capital. Public support typically shifts from broad deployment incentives to targeted de-risking and system enablers, as markets deepen. Finally, technologies enter Market Expansion, where adoption becomes widespread, and the innovation is embedded as a mainstream option.

This stage-based framing also helps contextualise this year’s budget signals on strategic technologies. CCUS, for example, appears to be at an early stage of the diffusion curve in India, as deployment remains limited and there are no commercial-scale dedicated CCUS projects. One of the main impediments to investment in CCUS projects is the absence of policy incentives and framework(s). That is why, in early-stage settings, support usually requires more than funding. It also needs clear frameworks that reduce uncertainty and enable first-of-a-kind projects.

The proposed rare-earth corridors and the focus on critical minerals indicate an emphasis on building the front end of clean-tech supply chains. This entails strengthening the mining, processing, and manufacturing of key inputs that underpin batteries, solar panels, and other clean technologies. If these inputs are cheaper and more reliably available in India, downstream technologies can scale faster.

Customs-duty relief for nuclear equipment also works mainly through costs. It can reduce the upfront price of key components. However, nuclear expansion is typically a slow process because projects take years and require strong delivery capacity and institutions. Duty cuts for lithium-ion cells and inputs for solar-panel glass support technologies and supply chains that are already scaling. Here, the constraints are different. The priority is to further reduce costs, scale manufacturing quickly, and ensure the power system can absorb higher volumes. This includes adequate transmission, reliable distribution utilities, and the flexibility needed to integrate more solar and storage.

Why Instrument Choice Matters as Much as the Budget Amount

This year’s budget announcements show which technologies and supply chains the government is prioritising. The harder question is how to design instruments that translate that priority into scale. Diffusion outcomes depend not only on the instrument chosen, but on how it is designed and applied. Weisbach also argues that, in the context of climate policy, many apparent differences between instruments come from design assumptions, and the gains from getting design right can outweigh the gains from debating instrument labels. Put simply, it is less important whether something is called a subsidy, a tax break, or a regulation, and more important what it actually does on the ground; who it targets, what conditions apply, how long it lasts, and how predictable it is.

For clean technology diffusion, this means that policy must start with diagnosis. It needs to identify the most limiting bottlenecks at a technology’s current stage and then choose instruments that directly address them. For instance, if the constraint is early-stage uncertainty, support that builds proof and capability matters more. If the constraint is bankability, the priority shifts to reducing risk and improving revenue certainty. If the constraint is integration, the focus shifts to system readiness and enabling infrastructure. When budgetary allocations are aligned with stage-specific barriers, they are more likely to translate into faster and more effective diffusion.

Conclusion

Budget 2026-27 sets a direction of travel towards strategic technologies, domestic supply chains, and integration capacity. The next step is policy design; therefore, it must ensure that the instruments are appropriate for the stage each technology is in, and at the right scale, to relax the constraint that is holding it back. Achieving this alignment at an early stage improves the chances of faster diffusion and more durable outcomes.

Endnotes

- On-budget support means government support that is explicitly recorded in the government’s Budget documents and authorised through Parliament. That means, it shows up as a line item of expenditure in official budget papers. ↩︎