Research area: Climate Policy

Trade liberalisation meets carbon tariffs as India eyes EU market

Bonn Deadlock Puts Pressure on COP31—and on Climate Multilateralism

Bidding Goodbye to COP33: Has India Missed a Trick?

India’s Second NDC: Revisiting the Intensity of Climate Ambition

India has recently approved its second Nationally Determined Contribution (NDC) to the Paris Agreement, for the period 2031-35. This commitment, despite being announced nearly five months late, serves as an important signal of India’s intent to decarbonise and support global efforts to limit climate change. It also constitutes a critical pillar of the Agreement’s ratchet mechanism, designed to progressively scale up global climate action in a manner that is compatible with the principle of Common but Differentiated Responsibilities and Respective Capacities (CBDR-RC).

India’s original NDC in 2016 had been welcomed as representing significant climate action from a country that accounts for under 4% of historical emissions and whose per capita emissions are still under half the global average. It had three quantified targets and has easily surpassed the first two, enabling it to further tighten its subsequent targets. The original targets and their revisions are shown in Table 1 below.

| India’s NDC commitments | Submission year | Target year | 1. Emissions intensity reductions below 2005 levels | 2. Non-fossil-based electricity generating capacity shares | 3. Additional carbon sinks (GtCO2e) |

| INDC | 2016 | 2030 | 33-35% (surpassed) | 40% (surpassed) | 2.5-3.0 |

| Updated NDC | 2022 | 2030 | 45% | 50% | 2.5-3.0 |

| Second NDC | 2026* | 2035 | 47% | 60% | 3.5-4.0 |

Of these, the emissions intensity (EI) target is the only economywide measure of climate progress, and it encompasses all other decarbonisation actions, including those relating to its other NDC targets for increasing non-fossil-based electricity capacity and carbon sinks. This EI target is our focus in this article, to better contextualise it and understand the scale of ambition it represents.

Alignment with India’s emissions intensity trajectory

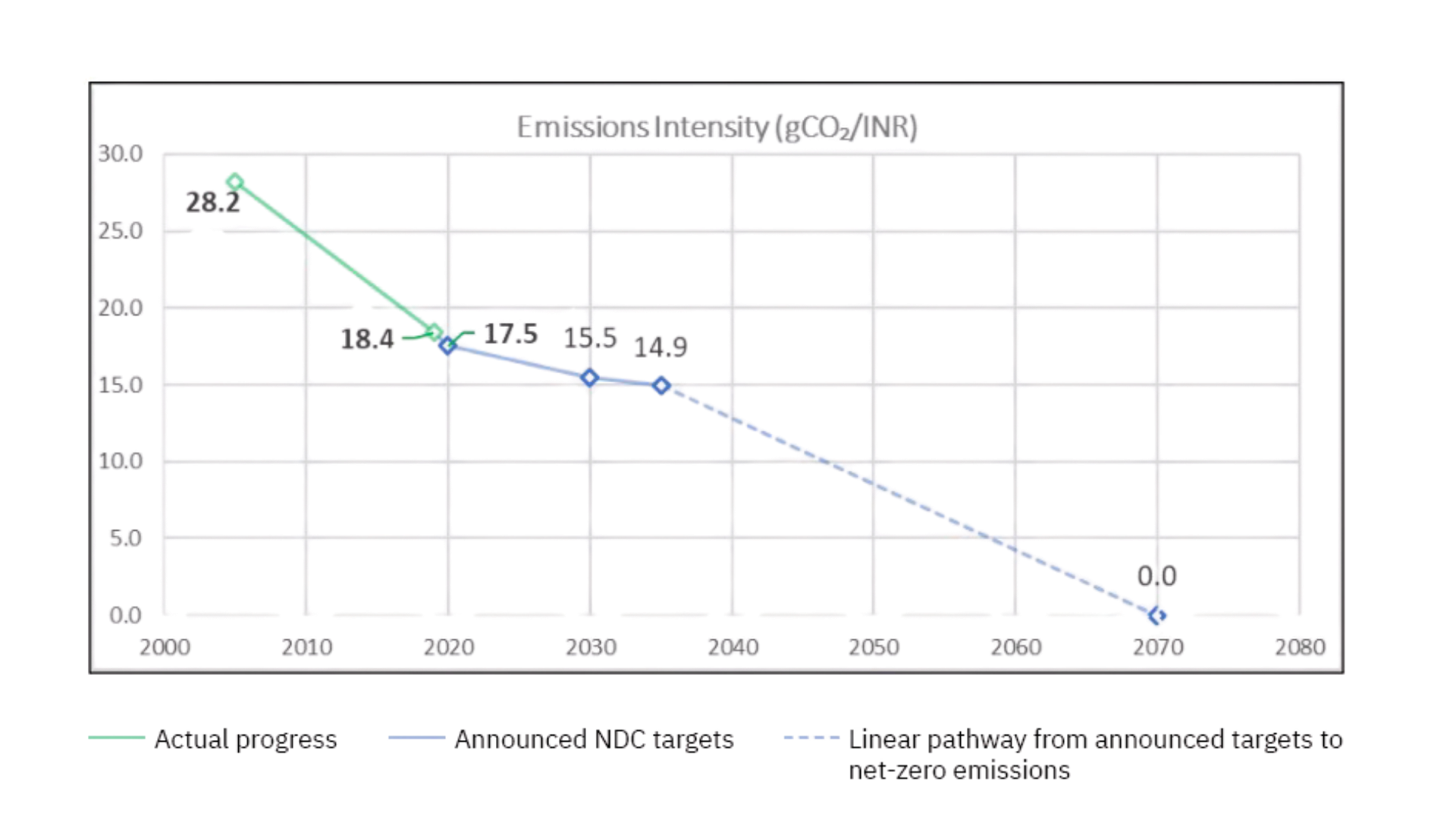

With India’s 2005 emissions estimated to be 1.64 GtCO2e1 and GDP at INR 58.1 trillion2, its 2005 EI was approximately 28.2 grams of CO2 equivalent (gCO2e)/rupee. Using the latest official emissions data from India’s Biennial Update Report to the UNFCCC and GDP data from MOSPI, we calculate India’s actual emissions intensity in 2019 and 2020 (see Figure 1), and observe that emissions intensity had already fallen by nearly 38% below 2005 levels by 2020, ten years ahead of its INDC commitment.

Source: Authors’ analysis.

As such, the updated NDC target of 2022 required only an additional 7% reduction in emissions intensity over 10 years, and the second NDC an even more modest 2% reduction over the next five. If India has linearly continued its 2005-2020 rate of EI reductions past 2020 – an admittedly simplistic and challenging assumption – it will already have reached its 47% target by 2024.

Alignment with Modelled Projections

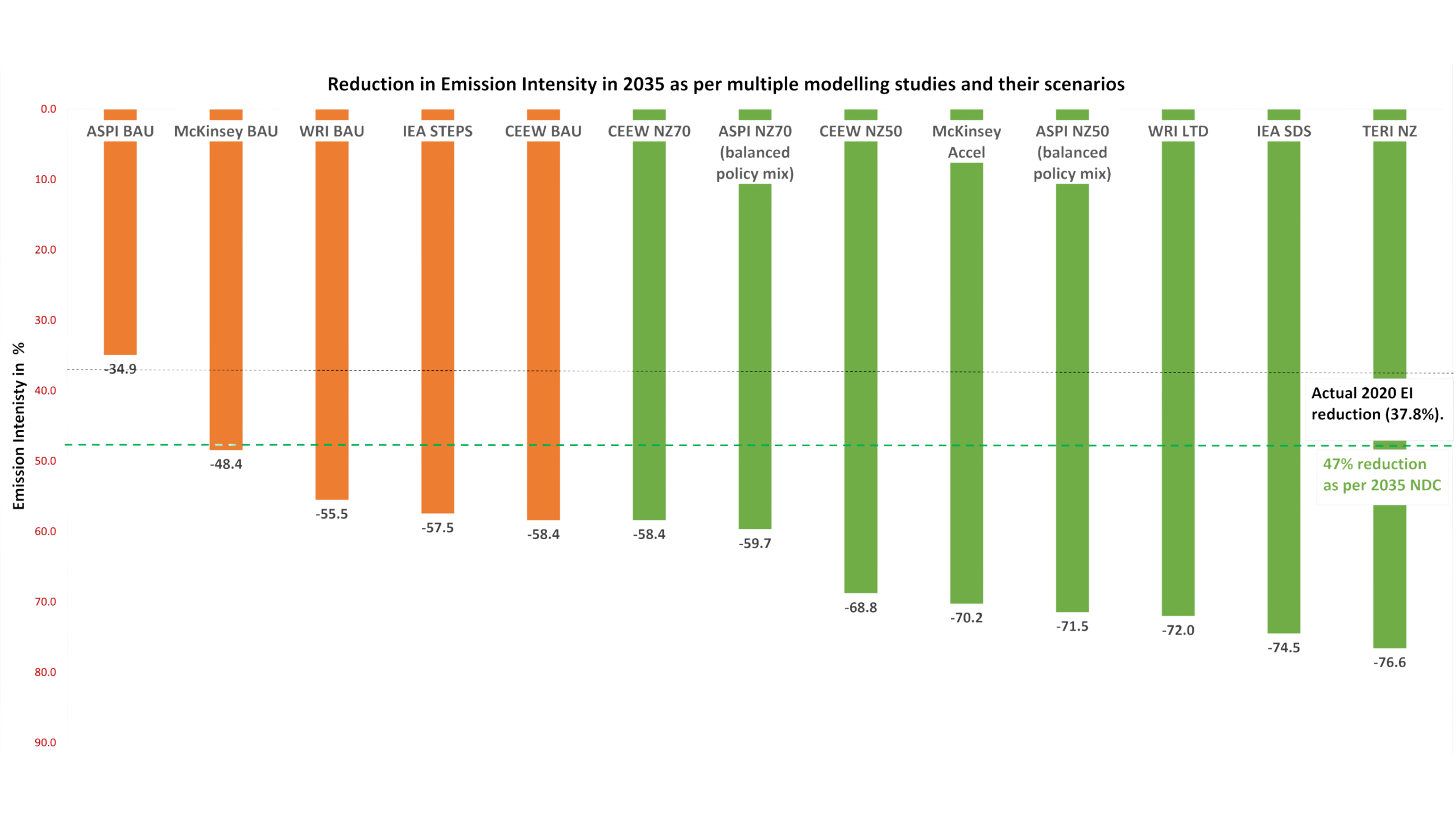

An assessment of 13 projected scenarios from five emissions-economy modelling studies that have explored India’s growth and emissions pathways3 further contextualises the recent pledge (Figure 2). Five of these projections (represented by the orange bars) can be interpreted as ‘reference’ scenarios, as they represent a continuation of trajectories that incorporate only existing decarbonisation policies and targets as of 2018-2020. The remaining eight are designed to represent scenarios based on additional policies that suggest possible pathways towards full decarbonisation in the second half of the century. The 47% intensity pledge appears to be consistent with – or even less ambitious than – decarbonisation pathways reflected in four of the reference scenarios here.

Source: Authors’ analysis.

Notes: (i) TERI-Shell and IEA only model emissions from the energy sector. (ii) IEA provides GDP estimates at 2019 prices; TERI-Shell GDP is based on MoSPI estimates at FY2011-12 prices. (iii) IEA GDP is converted using the exchange rate in its Annex B. (iv) An inflation adjustment is applied from the base year to rescale IEA estimates to FY2011-12 prices, based on a Ministry of Finance Cost Inflation Index.

Impacts on the Carbon Budget

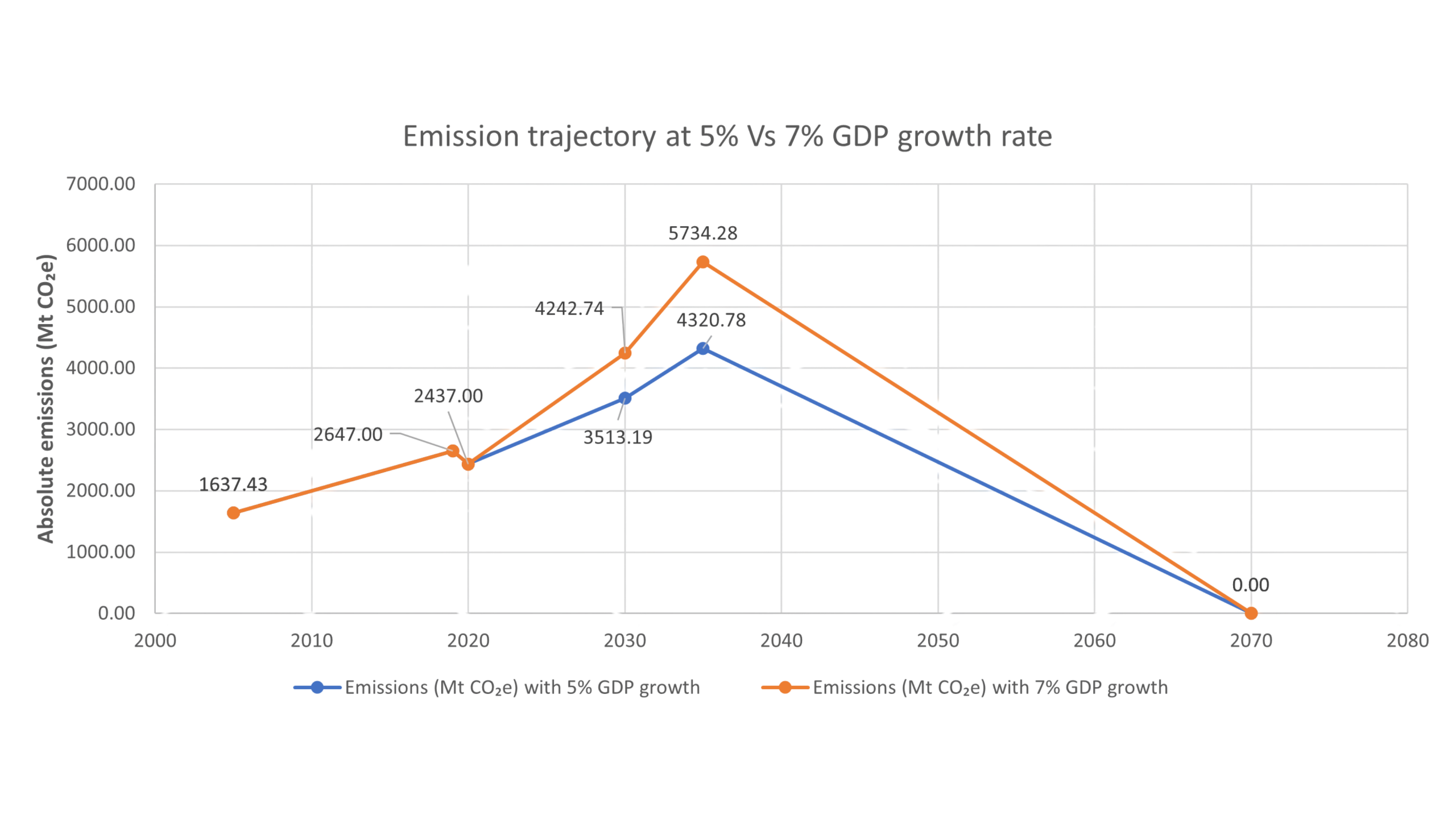

If India were to indeed limit its emissions intensity reductions to 47% by 2035, then – assuming an immediate and linear subsequent decline towards its 2070 net-zero target under constant 5% and 7% GDP growth rates – it would use up between 123 and 158 GtCO2e of the global carbon budget, respectively (Figure 3).

Source: Authors’ analysis.

With a remaining global carbon budget of only 400 GtCO2e as of 2020 to stay within the 1.5°C limit, India could thus exhaust up to 30-40% of this amount alone, with the wiggle room it has created for itself.

Drivers and Implications

While our analysis of the 2022 targets notes that the intensity pledge may serve as an ex-post reflection upon the feasibility of a set of regularly enhanced climate policies, and may represent a conservative underestimate aimed at overachieving its targets, these comparisons suggest that India’s stated climate ambition for the 2030-2035 period is proportionally modest, and is significantly scaled back from earlier efforts.

This is particularly noteworthy given that India’s emissions grew only 0.7% in 2025, while its GDP growth for the same year was forecast at 7.3%, pointing to a single-year emissions-intensity reduction of 6.6% – meeting nearly the entirety of the distance to the updated 2030 target in a single year alone.

The modest ambition of this target may, in large parts, be a product of the moment. The United States’ withdrawal from the Paris Agreement and receding climate finance commitments from other developed economies have weakened faith in the multilateral climate architecture. Parallel unilateral measures such as the EU’s Carbon Border Adjustment Mechanism – widely viewed in the Global South as protectionist – have further eroded trust in the Global North. In this context, India’s willingness to raise its stated ambition at all is of diplomatic significance, signalling its continued commitment to the Paris framework even in the face of real or perceived inaction by others.

At the same time, it creates more wiggle room for India to scale back its climate actions, and, given its misalignment with India’s own net-zero commitment and its potentially significant impacts on the carbon budget, may be viewed with concern. The argument for more ambitious action has never been stronger. India ranks among the world’s most climate-vulnerable nations, with over 85% of its districts exposed to extreme climate events. Further, in an era of emerging deglobalisation and greater supply chain uncertainties, the strategic case for energy self-sufficiency – enabled by greater domestic clean tech innovation and manufacturing capabilities – has acquired salience that extends beyond climate considerations.

An emerging vacuum has created an opportunity for India to step more decisively into a leadership role in global climate diplomacy, in a manner that is consistent with its own needs. A more ambitious mid-term signal could have cemented that role; instead, the new target represents a missed strategic opportunity and has opened up space for criticism, not unlike the global response to COP26.

The key question now is whether stated ambition is at all the driver of climate action, and whether India’s implementation once again significantly outpaces its stated ambition.

Endnotes

- Linearly interpolating between the 2000 and 2007 values ↩︎

- All GDP values are at 2011-12 prices ↩︎

- Each study used different inputs and assumptions relating to data sources, currencies, exchange rates, growth rates, base years, and other parameters. Although we attempted to harmonise estimates to a common baseline, insufficient clarity on modelling processes may limit the direct comparability of these studies. ↩︎

Global Climate Justice and the Future of Air Quality Co-Benefits in Low-Income and Middle-Income Countries: An Energy, Climate, and Health Modelling Study

Summary

Despite the need to limit climate change and transition to low-carbon energy, there is disagreement about how to share the burden of reducing CO2 emissions. Different approaches to global mitigation are assessed in this paper, accounting for three key factors: avoided climate harms, health (co)benefits from improved air quality, and the economic cost of CO2 policies. The approaches are then ranked according to different preferences for inter-generational and intra-generational equity.

Methods

We compare a reference scenario to three scenarios that limit warming to 2°C: one through least cost, one that shifts mitigation burden towards higher-income countries (referred to as the international equity scenario), and a third that is identical to international equity, but within which low-income and middle-income countries (LMICs) also adopt air quality policies to reduce air pollution to the levels that occur in least-cost. Emissions and policy costs are modelled with Global Change Analysis Model, air quality with GEOS-Chem, health impacts with the Global Exposure Mortality Model, and climate benefits with Greenhouse Gas Impact Value Estimator.

Findings

Climate action to limit global warming to 2°C results in more than 13·5 million avoided premature deaths from air pollution between 2020 and 2050, mostly in middle-income countries. Opting for the least-cost scenario rather than international equity reduces the mitigation burden for LMICs but also reduces their health co-benefits by several million deaths, highlighting a trade-off between mitigation effort (an important component of climate justice) and the urgent need to reduce environmental health burdens in LMICs. The extent to which equity is prioritised determines what to do about that trade-off; as more priority is given to lower-income countries, the international equity scenario is preferred. The most favourable scenario is the combined international equity and air quality scenario, whereby higher-income countries pay more climate mitigation costs, and LMICs use the cost savings to implement conventional air quality controls that offset foregone health co-benefits.

Interpretation

Justice-centred climate mitigation strategies must ensure that LMICs do not miss an opportunity to realise transformative reductions in air pollution.

India’s Energy Storage RD&D Bet: Why Batteries Dominate, and What That Means for the Future

Energy storage has emerged as a cornerstone technology for clean energy transitions globally. As power systems incorporate higher shares of variable renewable energy, maintaining reliability requires the ability to balance supply and demand across time. In India, where the target is 500 GW of non-fossil electricity capacity by 2030, this balancing challenge is becoming increasingly central. India’s energy storage requirement is expected to rise five-fold, with some projections suggesting 411.4 GWh by 2031–32, underscoring the scale and pace at which storage technologies will need to be developed and deployed. To adequately support high renewable penetration, system adequacy, and grid stability, grid-scale storage power capacity could reach up to 178 GW by mid-century, according to net-zero-consistent power-system modelling.

Energy storage technologies differ not only in the medium used to store energy, but also in the time scales, services, and system roles they are designed to perform, as well as the required research, development and demonstration (RD&D) needs. For instance, electrochemical storage1 dominates short- to medium-duration (15 minutes to <8 hours) applications where fast response, modularity, and ease of deployment are critical. Meanwhile, mechanical2, thermal3, and chemical4 storage technologies tend to serve longer-duration (> 8hours to days) or system-level roles, such as bulk energy shifting, inertia provision, or seasonal balancing, but are often more site-specific and infrastructure-intensive. In parallel, enabling layers, including power electronics, control systems, and software, cut across storage technologies and play a critical role in determining how effectively storage assets interact with the grid. These technologies differ from most other clean energy technologies in three ways.

Firstly, storage technologies do not generate energy; they provide flexibility. Their value lies in services such as peak shaving, frequency regulation, voltage support, reserve provision, and congestion management. As a result, storage performance cannot be assessed independently of the power system in which it operates. This contrasts with solar or wind technologies, where performance improvements are largely intrinsic to the device.

Secondly, storage technologies operate across multiple time scales. Storage must respond in milliseconds to stabilise the grid, operate over a few hours to shift solar power to evening peaks, and potentially store energy for longer periods in the future, particularly to manage multi-day renewable variability or extended supply shortfalls. Because no single technology can meet all these needs, storage RD&D naturally spans multiple approaches rather than converging on one solution.

Lastly, current storage technologies face a distinctive degradation problem. Unlike generation assets, storage systems, especially batteries, degrade with every charge–discharge cycle and even when they are not in use, requiring continuous RD&D to manage performance loss, safety risks, and lifespan reduction. These challenges are further amplified in India, where temperatures frequently exceed 40°C. For instance, a lithium-ion battery stored for one year at 40°C will drop to 65% of its full capacity even when stored and left unused.

These differences are not merely technical; they shape how storage RD&D is structured and funded. Public portfolios inevitably reflect choices about which system needs are prioritised and which technologies are considered ready for scale. Examining India’s public storage RD&D portfolio, therefore, offers insight into how the country is balancing near-term deployment needs with longer-term system transformation.

What India’s storage RD&D portfolio signals

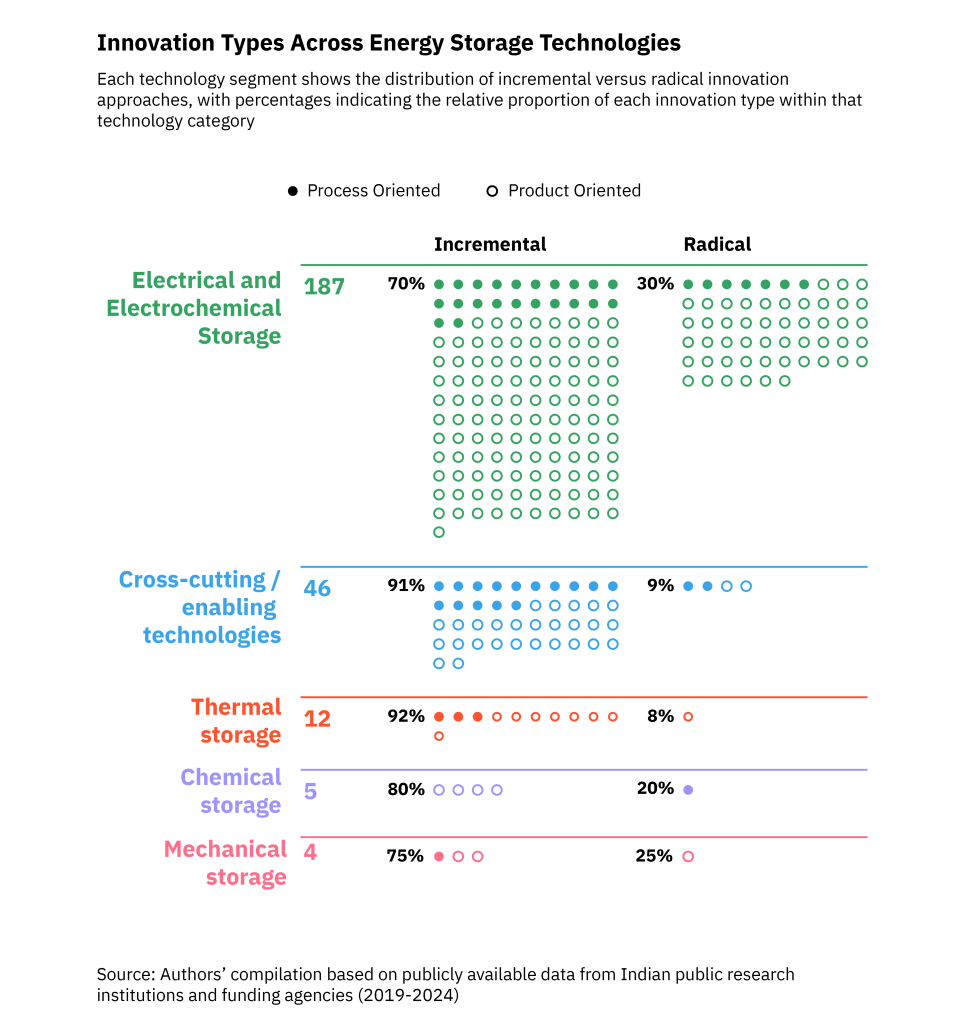

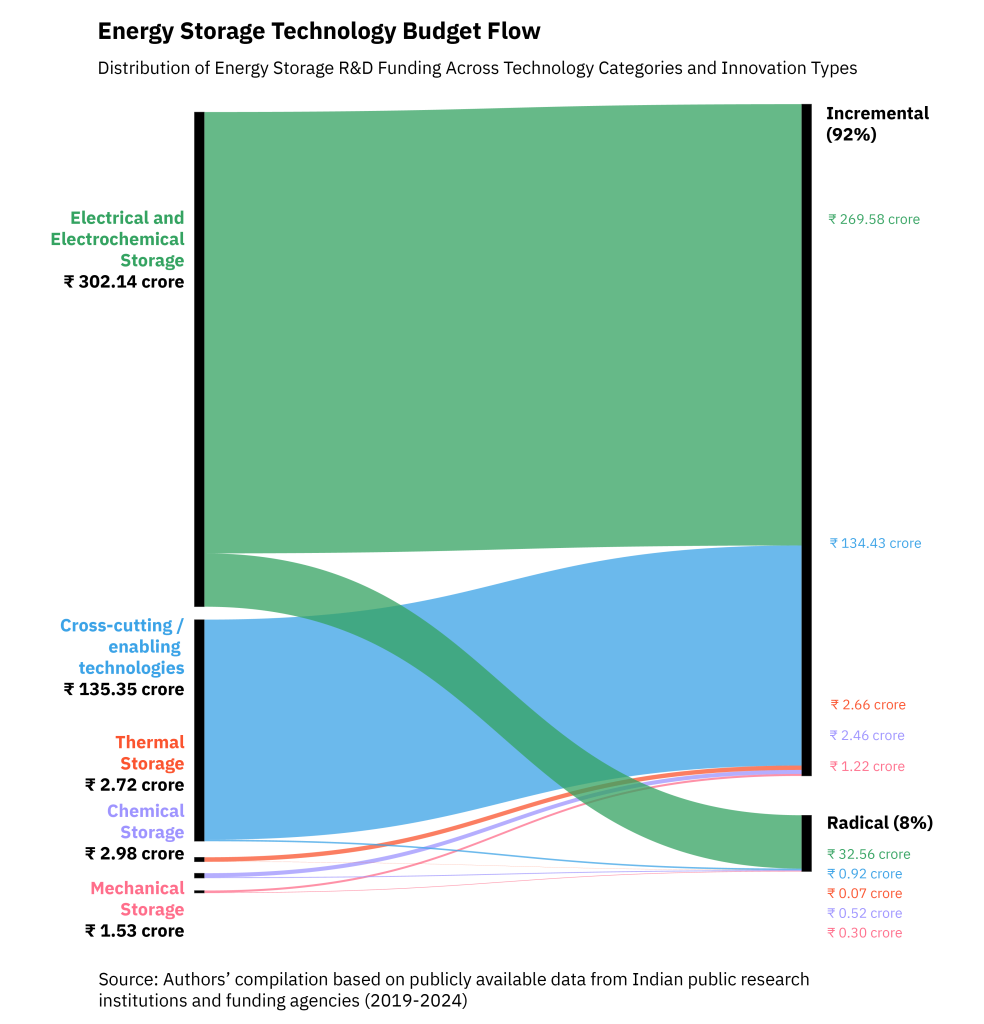

Our review of India’s public energy storage RD&D portfolio reveals a highly concentrated innovation strategy, centred overwhelmingly on electrochemical batteries and shaped by near-term system needs and industrial priorities. Our analysis focuses on publicly funded energy storage RD&D, given its central role in shaping technology trajectories, early-stage research, risk-sharing, and capability-building in India. At the same time, private firms are increasingly active with a growing start-up landscape emerging across the battery energy storage systems (BESS) value chain, from alternative chemistries and battery pack manufacturing to battery management systems (BMS) and battery-as-a-service models, signalling growing private-sector innovation alongside deployment.

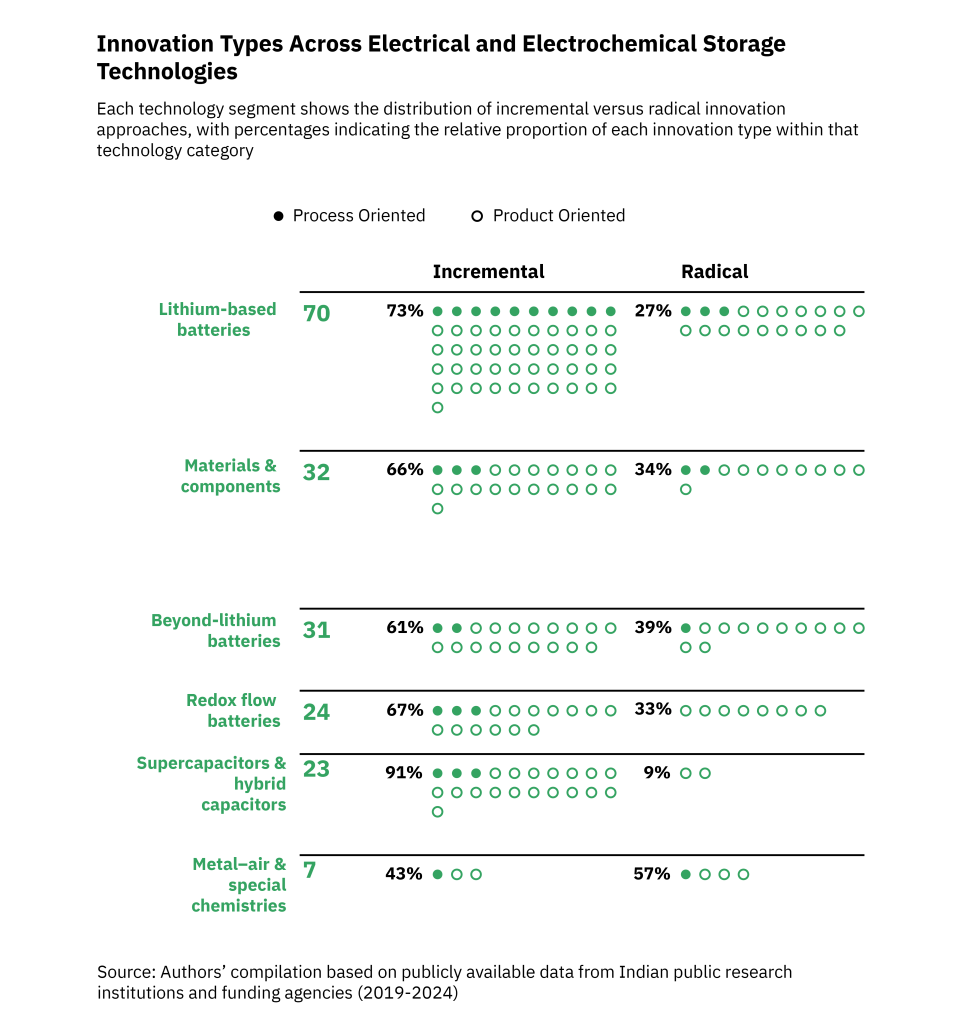

Across the portfolio of over 250 projects, electrochemical and electrical account for more than four-fifths5, with lithium-ion technologies forming the core. These projects focus primarily on incremental improvements to electrode materials, electrolytes, thermal stability, and cycle life, which influence performance, safety, and manufacturability. This emphasis reflects the dual role batteries play in India’s transition: they are both critical to electric mobility and as the most immediately deployable option for short-duration grid storage. While electric mobility and stationary storage batteries differ in performance requirements and, in some cases, chemistry choices, there are important areas of industrial overlap. Cell manufacturing, materials processing, pack assembly, battery management systems, and power electronics form a shared capability base. As India scales up advanced chemistry cell (ACC) manufacturing to meet demand across mobility and power sectors, learning effects and industrial spill-overs are likely to shape innovation trajectories in both domains.

While lithium-ion clearly dominates the portfolio, a smaller but visible set of projects explores alternative chemistries, including sodium- and aluminium-based systems grouped under the beyond-lithium battery category6 in the visual above, as well as redox flow batteries7. Their presence indicates growing awareness of geopolitical and mineral constraints, cost pressures associated with lithium-based systems, and of leveraging India’s relative advantage in sodium availability. Efforts are aimed towards reducing costs, improving efficiency, and developing India-centric designs. However, research into these technologies largely mirrors lithium-ion research in its orientation, focusing on device- and component-level innovation such as materials synthesis and performance benchmarking, rather than being embedded in a broader strategy for long-duration or grid-specific storage applications.

Public institutions such as Indian Institutes of Technology (IITs), Indian Institute of Science (IISc), Bengaluru, Central Electrochemical Research Institute (CECRI), and International Advanced Research Centre for Powder Metallurgy and New Materials (ARCI) are active across battery-focused research areas, alongside DST-supported projects on alternative chemistries and materials.

Beyond batteries, the portfolio thins out rapidly. Thermal energy storage8 appears in a small but meaningful subset of projects, suggesting some engagement with non-battery storage pathways. Yet these projects remain largely disconnected from discussions around industrial heat, renewable integration, and system flexibility, and are treated as standalone research topics.

More striking, however, is the near-absence of long-duration storage technologies. Project-level engagement with pumped hydro9 innovation, compressed air energy storage10, or gravity-based systems11 is minimal. This is notable given India’s significant pumped hydro potential of 176 GW and emerging concerns around grid inertia as solar penetration increases. This pattern does not necessarily imply that long-duration storage is unimportant. Rather, many of these technologies are highly site-specific and infrastructure-intensive, with feasibility shaped more by geography, land and water availability, permitting, and system planning than by laboratory-scale or component-level innovation. As a result, these technologies tend to be approached primarily as planning and project development challenges, rather than as domains where sustained public RD&D is viewed as the binding constraint.

Is India’s battery-first approach to storage a problem?

This focus on batteries raises a familiar question we have explored in earlier blogs on solar energy and green hydrogen in this series: Does India risk narrowing its innovation options by focusing so heavily on batteries? Or is this emphasis a rational response to India’s needs and global technology trajectories?

India’s battery-centric approach is not an outlier. Globally, BESS accounts for the overwhelming majority of new storage deployments and RD&D investment through 2030. In 2025, global investment in batteries for power sector storage is projected to have exceeded USD 66 billion with total installed battery storage capacity reaching 258 GW. Meeting the 2030 goal of tripling renewable energy will require a six-fold expansion of energy storage worldwide, with batteries expected to account for nearly 90% of new capacity additions and other technologies providing supplementary support. Such rapid scaling is largely enabled by declining battery costs. Utility-scale battery storage costs in 2024 fell to about USD 192/kWh, a roughly 93% decline since 2010, making batteries the most competitive option for short- to medium-duration storage.

Even in countries actively funding long-duration energy storage research, batteries continue to dominate near-term deployment because they are modular, quick to deploy, and compatible with existing grid architectures. China illustrates this pattern, combining large investments in pumped hydro with a near fourfold expansion in battery storage capacity in recent years. Similarly, Australia has rapidly expanded BESS but is investing heavily in non-battery storage in parallel, most notably through large pumped hydro projects designed to deliver long-duration energy shifting and system adequacy.

India’s energy storage RD&D strategy can therefore be seen as reflecting a near-term pragmatic reading of current system needs, global cost curves, and institutional constraints rather than a judgment about the technologies that will matter over the full course of the energy transition. By focusing on batteries, India is prioritising technologies that are commercially viable in the short-term, aligned with EV demand, and capable of scaling quickly to support renewable integration.

The question, therefore, is not whether India should shift away from batteries today but whether its storage innovation ecosystem retains the capacity to adapt as system needs evolve. Given current system conditions, rapid renewable scale-up, and the need for short- to medium-duration balancing, batteries remain the most practical and scalable storage option. The challenge for storage RD&D is not about correcting a misallocation in the present, but about ensuring that alternative pathways are not unintentionally side-lined as the power system becomes more complex beyond the early 2030s. In that sense, storage innovation is less about choosing a single winner and more about maintaining a portfolio that can respond to changing technical, economic, and system realities.

This blog is part of our Clean Energy RD&D Insights series, examining India’s evolving clean energy innovation landscape. Read the other blogs on green hydrogen here and solar energy here. We would also like to thank Kunal Agnihotri for his help in designing the visuals for this piece.

Endnotes

- Electrochemical energy storage systems store and release electricity through reversible chemical reactions within battery cells (e.g., lithium-ion, sodium-ion, redox flow) ↩︎

- Mechanical storage systems convert electrical energy into mechanical potential or kinetic energy (e.g., pumped hydro, compressed air, flywheels, gravity systems) ↩︎

- Thermal energy storage systems store energy as heat or cold in a medium (e.g., molten salts, water, phase-change materials) for later use in power generation or direct thermal applications ↩︎

- Chemical storage systems convert electricity into chemical energy carriers (e.g., hydrogen, synthetic fuels, ammonia) through processes such as electrolysis ↩︎

- In this analysis, electrical and electrochemical storage technologies are grouped together because they share similar innovation characteristics and RD&D pathways. Both rely on advances in materials science, power electronics, and system integration, and are typically deployed for short- to medium-duration applications requiring fast response times. In India’s public RD&D portfolio, these technologies are also funded, evaluated, and implemented through similar institutional and programmatic channels, making it analytically meaningful to examine them together ↩︎

- Beyond-lithium batteries category includes multiple chemistries such as sodium- and aluminium-based systems. These are grouped together as they represent alternative chemistries within broadly similar battery architectures. These technologies often target the same applications as lithium-ion systems, draw on comparable manufacturing processes, and face similar RD&D challenges related to materials performance, cost reduction, and scalability. Redox flow batteries and metal–air systems are treated as separate categories because they differ more fundamentally in design, operating principles, and innovation pathways ↩︎

- Besides lithium-ion batteries, flow batteries could emerge as a breakthrough technology for stationary storage as they do not show performance degradation for 25-30 years and are capable of being sized according to energy storage needs with limited investment ↩︎

- Thermal Energy Storage captures and stores heat or cold in a medium (like water, rock, or salt) for later use, balancing energy supply and demand ↩︎

- Pumped storage hydropower a large-scale energy storage method that uses two reservoirs at different elevations to act like a giant rechargeable battery, storing surplus electricity by pumping water uphill and releasing it downhill through turbines to generate power when needed ↩︎

- Compressed Air Energy Storage stores excess electricity by compressing air and storing it in underground caverns or tanks, releasing it later to drive turbines and generate power, effectively acting like a large battery ↩︎

- Gravity-based energy storage systems store excess electricity by lifting heavy masses (like concrete blocks or water) and release it by allowing them to fall, converting potential energy back into power using a generator, acting as a sustainable, long-lasting alternative to batteries ↩︎

From Budget Announcements to Outcomes: Why Instrument Choice and Design Will Decide What Scales

India’s Union Budget announcements are an important annual signal of where the Union government is committing its scarce on-budget1 resources, such as subsidies, grants, and public investment, revealing the priorities and trade-offs it is willing to make. In particular, the 2026–27 announcement signals what the government intends to support domestically in the clean energy transition. Four announcements stand out. First, a $2.2bn push for carbon capture, utilisation and storage (CCUS), positioned as support for industrial decarbonisation and intended to reach multiple hard-to-abate sectors. Second, a renewed focus on critical and rare earth minerals, including a proposal to establish dedicated rare-earth corridors in Odisha, Kerala, Andhra Pradesh, and Tamil Nadu to promote mining, processing, research, and manufacturing. Third, customs-duty relief on imports of nuclear power equipment, with the exemption extended through 2035. Fourth, duty cuts for lithium-ion cells for battery storage and inputs for solar-panel glass manufacturing, thereby lowering input costs in key clean-tech supply chains. Alongside these, power-sector spending continues to point toward grid and integration enablers, including efforts often discussed through programmes like the Green Energy Corridor.

Taken together, these measures signal a push to strengthen domestic supply chains and the backbone needed for the clean energy transition. They may lower input costs, support domestic value chains, and invest in infrastructure that must carry a higher share of clean power. Realising this ambition will require an increase in overall funding; the key question, then, is what form that support would take and whether it is suited to addressing the relevant bottlenecks.

A Technology Diffusion and Finance Framework

Our research on clean technology diffusion begins with the premise that financing barriers and the types of financial support required vary across stages of their diffusion. What hinders a technology early is often not what holds it back later. To study this, we draw on the innovation systems approach, which assumes that any technology needs a supporting ecosystem to diffuse. It focuses on the ecosystem of actors (firms, researchers, financiers, government) and the rules and infrastructure (standards, regulation, procurement, networks) that together determine whether a new technology can develop, prove itself, and scale. Using this approach, we then map the range of policy instruments (fiscal and non-fiscal, as well as financial and non-financial) that governments use to support diffusion.

Existing literature commonly organises diffusion into five stages along an S-curve, from early research to market saturation. The innovation process typically begins with a Solution Search phase, when there are significant uncertainties about the technology’s future market potential. Private capital is hard to attract at this stage. Public support, therefore, tends to focus on early research and development – through grants and subsidies – to explore options and identify potential new solutions. Once viable options emerge, they proceed to the Proof of Concept stage, in which pilot projects are implemented to test feasibility in real-world conditions. If those efforts succeed, technologies enter the Early Adoption phase. At this stage, they have cleared major technical hurdles but are not yet commercially established. Policy support often focuses on enabling first-market entry and encouraging initial uptake. As deployment grows, System Integration becomes critical, a phase when the projects become attractive to institutional investors. The priority shifts to building enabling infrastructure and market frameworks so projects can scale reliably and attract larger pools of private capital. Public support typically shifts from broad deployment incentives to targeted de-risking and system enablers, as markets deepen. Finally, technologies enter Market Expansion, where adoption becomes widespread, and the innovation is embedded as a mainstream option.

This stage-based framing also helps contextualise this year’s budget signals on strategic technologies. CCUS, for example, appears to be at an early stage of the diffusion curve in India, as deployment remains limited and there are no commercial-scale dedicated CCUS projects. One of the main impediments to investment in CCUS projects is the absence of policy incentives and framework(s). That is why, in early-stage settings, support usually requires more than funding. It also needs clear frameworks that reduce uncertainty and enable first-of-a-kind projects.

The proposed rare-earth corridors and the focus on critical minerals indicate an emphasis on building the front end of clean-tech supply chains. This entails strengthening the mining, processing, and manufacturing of key inputs that underpin batteries, solar panels, and other clean technologies. If these inputs are cheaper and more reliably available in India, downstream technologies can scale faster.

Customs-duty relief for nuclear equipment also works mainly through costs. It can reduce the upfront price of key components. However, nuclear expansion is typically a slow process because projects take years and require strong delivery capacity and institutions. Duty cuts for lithium-ion cells and inputs for solar-panel glass support technologies and supply chains that are already scaling. Here, the constraints are different. The priority is to further reduce costs, scale manufacturing quickly, and ensure the power system can absorb higher volumes. This includes adequate transmission, reliable distribution utilities, and the flexibility needed to integrate more solar and storage.

Why Instrument Choice Matters as Much as the Budget Amount

This year’s budget announcements show which technologies and supply chains the government is prioritising. The harder question is how to design instruments that translate that priority into scale. Diffusion outcomes depend not only on the instrument chosen, but on how it is designed and applied. Weisbach also argues that, in the context of climate policy, many apparent differences between instruments come from design assumptions, and the gains from getting design right can outweigh the gains from debating instrument labels. Put simply, it is less important whether something is called a subsidy, a tax break, or a regulation, and more important what it actually does on the ground; who it targets, what conditions apply, how long it lasts, and how predictable it is.

For clean technology diffusion, this means that policy must start with diagnosis. It needs to identify the most limiting bottlenecks at a technology’s current stage and then choose instruments that directly address them. For instance, if the constraint is early-stage uncertainty, support that builds proof and capability matters more. If the constraint is bankability, the priority shifts to reducing risk and improving revenue certainty. If the constraint is integration, the focus shifts to system readiness and enabling infrastructure. When budgetary allocations are aligned with stage-specific barriers, they are more likely to translate into faster and more effective diffusion.

Conclusion

Budget 2026-27 sets a direction of travel towards strategic technologies, domestic supply chains, and integration capacity. The next step is policy design; therefore, it must ensure that the instruments are appropriate for the stage each technology is in, and at the right scale, to relax the constraint that is holding it back. Achieving this alignment at an early stage improves the chances of faster diffusion and more durable outcomes.

Endnotes

- On-budget support means government support that is explicitly recorded in the government’s Budget documents and authorised through Parliament. That means, it shows up as a line item of expenditure in official budget papers. ↩︎

India’s AI Push Is Quietly Draining Its Energy, Resources, and Space

India’s Green Hydrogen Push: Engineering for Today or Innovating for Tomorrow?

Green hydrogen is often positioned as India’s next clean energy frontier. In 2023, the country set a goal to produce 5 million metric tons of green hydrogen annually by 2030, under the National Green Hydrogen Mission (NGHM). The mission is framed as the centrepiece of India’s vision to achieve net-zero emissions by 2070, reduce emissions and fossil fuel imports, and position itself as a global leader in green hydrogen technology1.

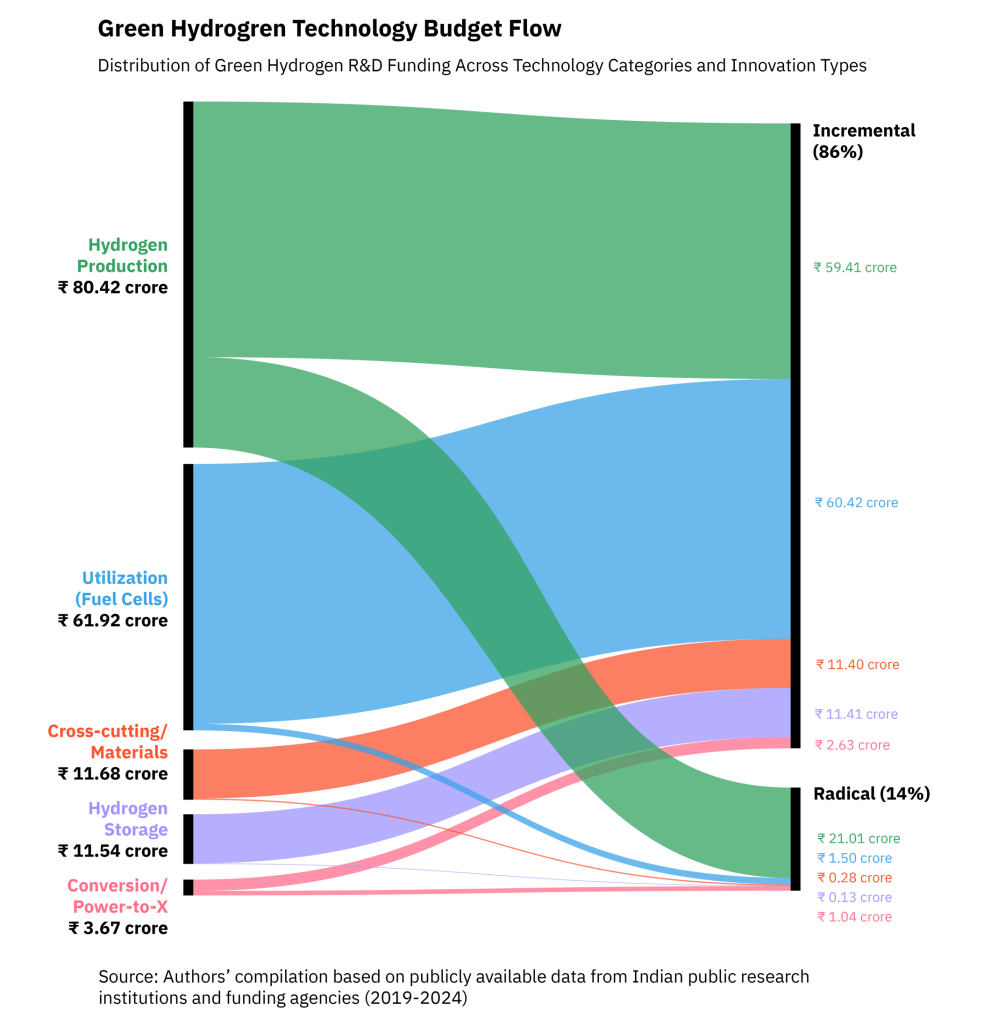

The NGHM recognises the importance of innovation and outlines a three-tiered framework that spans near-term, industry-linked projects, mid-term component advances, and long-horizon, high-risk research to build future technological capabilities. It has proposed a Strategic Hydrogen Innovation Partnership (SHIP) to pool public and private resources and earmarked ₹400 crore ($47 million) for research and development (R&D). However, this represents only about 2% of the total mission outlay of ₹19,744 crore ($USD 2.3 billion). Additionally, ₹1,466 crore ($172 million) has been allocated for pilot projects in sectors like steel, mobility, and shipping. Most of the funding is allocated to the Strategic Interventions for Green Hydrogen Transition (SIGHT) programme, which has demarcated ₹17,490 crore ($2.1 billion) in incentives to scale electrolyser manufacturing and green hydrogen production.

While private investment is beginning to flow into green hydrogen production and manufacturing, particularly through incentive schemes such as SIGHT, early-stage research and demonstration activities continue to be anchored in public funding and public-sector institutions in India. As of early 2025, 23 R&D projects have been awarded grants under the NGHM across areas such as hydrogen production from biomass, hydrogen applications, and non-biomass hydrogen production routes. The limited R&D allocation raises questions about whether India’s publicly funded green hydrogen R&D efforts are sized and timed to deliver the long-term technological and market leadership the NGHM envisions.

Why Hydrogen Innovation is Different

Hydrogen is a multi-system technology involving electricity, water, materials, and industrial processes. Unlike solar or battery technologies, which can advance through stand-alone improvements in modules, materials, or manufacturing, hydrogen innovation relies on the seamless interaction of production, storage, transport, and end-use. Each step in the process is deeply interconnected, and efficiency gains in one part can be lost if the rest of the chain is not aligned. For instance, a breakthrough in electrolysis means little without affordable storage or reliable industrial demand. Progress, therefore, takes longer, costs more, and relies on close coordination between researchers, engineers, and industries.

What the Public R&D Portfolio Shows

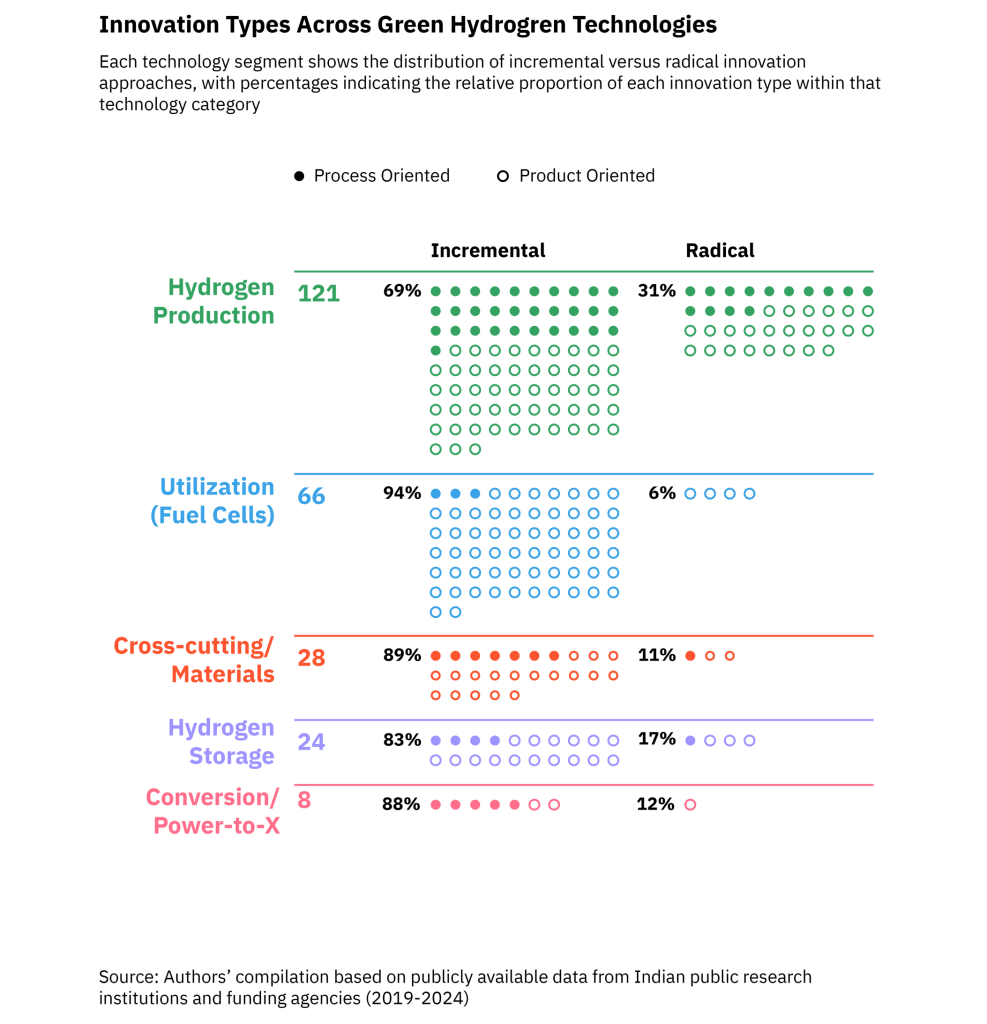

Drawing on our review of almost 250 publicly-funded hydrogen research projects between 2019-24, across Indian Institutes of Technology (IITs), Council of Scientific and Industrial Research (CSIR) laboratories, national institutes, and other government-supported centres, a clear pattern emerges. Most of India’s hydrogen research activities are aimed at incremental improvements, to address crucial knowledge gaps, build domestic capabilities, and reduce production costs. This mirrors the pattern we noted in our analysis of solar R&D, where innovation has largely focused on making technologies more affordable and better adapted to Indian conditions rather than creating frontier breakthroughs. Incremental, cost-oriented innovation aligns with India’s comparative advantage – low renewable electricity costs, high solar irradiance, and a rapidly expanding transmission network – and points to an R&D portfolio oriented toward cost-competitive green hydrogen for domestic deployment and cost-sensitive export markets.

As seen in the figure above, much of the current focus lies in the development of electrolysers2 and fuel cells, the backbone of hydrogen production and conversion. Here, research is directed at membranes, catalysts, and stack optimisation across a range of chemistries, including proton exchange membrane (PEM)3, alkaline4, and solid oxide cells5. Scientists are working to reduce dependence on expensive metals such as platinum, improve membrane durability, and enhance performance under local operating conditions.

A related stream of incremental work focuses on integrating electrolysers with variable renewable power, which remains one of the most challenging aspects of hydrogen deployment globally. In India, some research institutions, such as IIT Madras and IIT Guwahati, are focused on developing solutions to manage intermittency and maintain grid stability as hydrogen production scales.

Nevertheless, the scale of funding constrains laboratory research from moving to the demonstration phase. Many projects fall within the ₹20–70 lakh ($23.5-82.3K) range, sufficient for exploratory research but not for pilot-scale demonstrations. Even the more ambitious efforts, such as the development of a 20 kW fuel cell system at the Indian Institute of Space Science and Technology (IIST), are small compared with the multi-million dollar and multi-megawatt demonstration projects already underway in other countries. For example, Japan’s Green Innovation Fund allocates between JP¥ 30–220 billion (₹1,700–12,500 crore) to individual hydrogen demonstration projects, and the US Department of Energy has been funding $10–150 million (₹80–1,200 crore) demonstration-scale projects. While India’s lower labour and operational costs allow the rupee to stretch further, the order-of-magnitude difference in resources remains striking.

Alongside these incremental efforts, a smaller set of radical projects explores new directions altogether. For instance, CSIR-AMPRI has piloted a hydrogen-powered desalination system, linking clean energy with water security. IIT Delhi and IIT Mandi are developing techniques to split water using sunlight as the primary energy input, reducing reliance on external electricity during operation. IIT Jodhpur and IIT Madras are exploring hydrogen–ammonia fuel blends for industrial applications, while IIT (BHU) Varanasi is testing new reformer designs for ultra-pure hydrogen production. These projects have the potential to define future technologies, but they remain at low technology readiness levels with limited funding support. For instance, a solar-to-hydrogen reactor project received under ₹5 lakh ($5882), underscoring the small scale of radical research.

While incremental work is concentrated upstream in production and conversion, and radical work appears in scattered pockets, the midstream aspects of storage, transport, and logistics remain India’s weakest link. This mirrors global trends with international assessments identifying midstream technologies as the least mature parts of the hydrogen value chain, requiring substantial R&D before large-scale deployment. The result is a research landscape where activity is clustered at the beginning and end of the value chain, but the infrastructure that connects them remains thin. The country is still developing basic capabilities in this area, and only a handful of projects address this gap, including CSIR-AMPRI’s ADHERE composite pressure vessels, IIT Ropar’s ceramic membranes for hydrogen purification, and IIT Bombay’s compressed hydrogen–fuel cell integration system. Geological surveys in Rajasthan have identified salt-cavern potential for large-scale storage, but structured pilots have yet to start.

Choosing a Direction

This brings us to a central question: What is India optimising for?

The current portfolio suggests competing objectives, each with its own implications. If the priority is cost reduction and affordability, as the dominance of incremental research implies, then R&D should be followed by large-scale deployment, localisation of components, and strong industrial pull. However, this approach is unlikely to create distinctive intellectual property or position India as a leader in research and innovation.

On the other hand, if the goal is technology leadership, which is consistent with the NGHM’s stated ambition, then India requires far greater coordination, stronger pathways to scale up, and multi-year funding for breakthrough technologies. This would also involve longer development cycles, higher uncertainty, and support for moonshot ideas that may or may not succeed. Such attempts are necessary to build future capabilities and competitiveness in cutting-edge technologies.

At present, the portfolio reflects neither approach fully. Instead, small investments are spread thinly across almost the entire value chain. This breadth without depth makes it challenging to build leadership, whether through scale-driven cost competitiveness or through breakthrough innovation.

The challenge ahead is not merely one of ambition but also of alignment – aligning both laboratory innovation with industrial demand and public investment with long-term strategy. Since the hydrogen landscape is still developing, the strategic choices India makes now about where to direct R&D and how to scale it will shape its long-term position far more than in mature sectors. This will determine whether India can become a country that not only deploys hydrogen but also designs the technologies that define it.

We would like to thank Kunal Agnihotri for his help in designing the visuals featured in this piece. This blog is part of our Clean Energy RD&D Insights series, examining India’s evolving clean energy innovation landscape. Read the other blogs in this series on energy storage here and solar energy here.

Endnotes

- Our piece titled, ‘Beyond the Hype: Opportunities and Limits of India’s Green Hydrogen Pursuit‘, explores the feasibility of this

↩︎ - Electrolysis is a technique that uses electric current to drive an otherwise nonspontaneous chemical reaction. One form of electrolysis is the process that decomposes water into hydrogen and oxygen, taking place in an electrolyser and producing green hydrogen. ↩︎

- Proton Exchange or Polymer Electrolyte Membrane (PEM) electrolyser: A specific water electrolysis technology which operates under acidic conditions using a polymer to separate the electrodes. ↩︎

- Alkaline hydrogen refers to hydrogen produced via alkaline water electrolysis, a mature, cost-effective method using electricity to split water into hydrogen and oxygen in an alkaline (basic) solution, offering a clean way to store renewable energy. ↩︎

- Solid oxide fuel cells (SOFCs) use a hard, non-porous ceramic compound as the electrolyte. SOFCs operate at very high temperatures—as high as 1,000°C (1,830°F). High-temperature operation removes the need for a precious-metal catalyst, thereby reducing cost. It also allows SOFCs to reform fuels internally, which enables the use of a variety of fuels and reduces the cost associated with adding a reformer to the system. ↩︎